How Does a Trustee Work in Arizona? Duties, Powers, and Practical Steps

Key Takeaways

A trustee is a person or entity appointed to hold, manage, and administer assets in a trust for the benefit of designated beneficiaries in the Arizona state. The trustee manages trust assets and trust property under the trust document, with strict fiduciary duty rules and possible personal liability if those rules are broken.

A trustee controls investments, pay bills, handles taxes, and makes income and principal distributions, but trustee must follow the terms of the trust, the trust agreement, and state law.

A trustee can be one of your family members, a trusted friend, an attorney, a corporate trustee, or a trust company.

Trustee choosing is one of the most important decisions in an estate plan because the right trustee must act in the best interest of the beneficiaries.

In Arizona, Citadel Law Firm helps clients draft trusts, select trustees, and guide a successor trustee through trust administration.

If you have been named trustee or are creating a trust, schedule a free consultation with Citadel Law Firm to answer questions before mistakes become expensive.

What Is a Trustee and How Do They Work Day to Day?

So, how does trustee work in plain English? A trustee holds legal title to trust assets and trust property, then manages them for beneficiaries according to the trust document and applicable law.

For example, a Chandler, Arizona couple in 2026 may place a home, bank accounts, an IRA, and other assets into a revocable living trust. While they are alive and competent, one spouse may serve as primary trustee. After incapacity or the grantor’s death, the successor trustee steps in, contacts financial institutions, gathers assets held in the trust, protects the home, and begins distributing trust assets when allowed.

A trust usually has three parties: the trust creator, also called the grantor or settlor; the trustee, who administers the trust; and the trust beneficiary or trust beneficiaries, who receive income, funds, property, or other benefits. Sometimes one person serves in more than one role.

How a trustee works depends on whether the trust is revocable or irrevocable and whether the grantor is alive. A trustee administers, manages, and distributes the assets in a trust after the grantor dies, while an executor administers and manages the estate of someone who has died, distributing the assets left to heirs through a will. Both trustees and executors have a legal responsibility to act in the best interest of the beneficiaries, but they are responsible for different parts of an estate. An individual can be appointed as both a trustee and an executor, but these roles have distinct responsibilities and functions in estate management.

On a daily basis, the trustee role may include reviewing account statements, approving distributions, speaking with a financial advisor, hiring a tax advisor, keeping detailed records, and preparing for future accountings.

Core Legal Duties of a Trustee (Fiduciary Duty Explained)

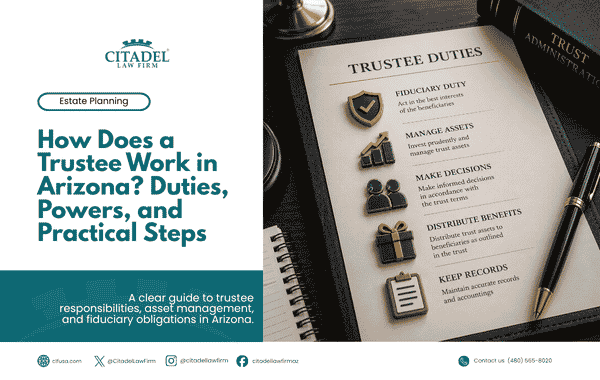

Fiduciary duty means the trustee must put personal interests and biases aside and act in the best interests of the beneficiaries. Arizona and other states impose trustee duties by statute and case law; for example, Arizona’s duty to inform and report appears in A.R.S. § 14-10813.

The duty to administer trust assets requires the trustee to follow the trust instrument, safeguard real estate, manage investment accounts, pay property taxes, insurance, HOA dues, and carry out certain duties with care. A trustee is responsible for properly managing all property and other assets placed in the trust for the beneficiaries, ensuring that the grantor’s wishes are fulfilled as outlined in the trust document.

The duty of loyalty requires the trustee to administer the trust solely in the beneficiaries’ interest. Trustees cannot self-deal, commingle trust funds with personal funds, misappropriate trust funds, or favor one beneficiary for personal reasons. Trustees can be held liable for breaches of their fiduciary duties, which may include misappropriation of trust funds or failing to act in the best interest of the beneficiaries.

The duty of impartiality matters when there are multiple beneficiaries. An older sibling trustee managing money for younger siblings must treat beneficiaries impartially and balance current and future beneficiaries, including future beneficiaries who may receive assets later.

The duty of prudence requires trustees to invest trust funds prudently to preserve capital and generate reasonable returns. That does not mean chasing the highest return; it means using reasonable modern portfolio concepts, considering risk, liquidity, income, and the trust’s purpose. A trustee may hire an investment manager, but the trustee is responsible for oversight.

The duty to inform and account means beneficiaries often have a right to see relevant parts of the trust document and receive reports showing income, expenses, compensation, and principal distributions. Trustees must keep detailed records of all transactions, including income and expenses, to ensure transparency and accountability in trust administration.

What Exactly Does a Trustee Do With Trust Assets?

In the first year after a death in 2026, a trustee may collect trust property, retitle accounts, pay final bills, file tax returns, and start distributions. Trustees must balance administrative tasks with strict legal obligations.

Common work includes:

-

Identifying and marshaling real estate, bank and brokerage accounts, business interests, and other assets.

-

Setting up new trust accounts and updating titles or signature authority.

-

Working with financial planning professionals, rebalancing investments, deciding between income and growth, and documenting tax decisions.

-

Making income and principal distributions or principal distributions under standards like health, education, maintenance, and support.

-

Coordinating with CPAs for the trust’s annual tax returns, Form 1041 when required, and tax laws affecting distributions.

Trustees must make distributions of income or principal strictly in accordance with the rules laid out in the trust document. Trustees are responsible for filing the trust’s annual tax returns and ensuring any applicable taxes are paid from the trust’s funds.

Trustees have the authority to hire and consult professionals to help manage the trust, but they remain ultimately liable for the trust’s management. Professional advice helps, but it does not erase fiduciary responsibility.

How Much Power Does a Trustee Have Over Trust Funds?

A trustee has broad control over trust funds and trust property, but that power is limited by the trust document and fiduciary law. In Arizona, A.R.S. § 14-10815 gives trustees broad powers unless the trust limits them.

Mandatory distributions require action, such as “pay all net income annually at age 25.” Discretionary distributions allow trustee’s discretion over if, when, and how much to distribute assets. Even then, the trustee may not use a trust solely for personal advantage.

Practical limits are real. Beneficiaries can request information, demand accountings, object to unreasonable decisions, or ask a court to remove a trustee. Modern estate plans may use a co trustee, co trustees, multiple trustees, or a trust protector to add oversight.

-

In Arizona, courts can surcharge a trustee personally, unwind improper transactions, reduce fees, or order removal if fiduciary duties are breached under rules such as A.R.S. § 14-10706.

Choosing the Right Trustee or Successor Trustee

Naming the right trustee or successor trustee can be as important as deciding who receives your inheritance.

Individual trustees, such as spouses, adult children, family members, or a trusted friend, may know the family well and cost less. The downside is family conflict, limited financial experience, or lack of time.

Professional options include a trust company, bank, corporate fiduciary, or attorney. Selecting a professional trustee may provide advantages such as impartiality and expertise, which can be beneficial in managing complex trusts and ensuring compliance with legal obligations.

A sole trustee can work for simple trusts, while multiple trustees or co-trustees may balance family insight with fiduciary services. The risk is gridlock if decision-making rules are unclear.

When choosing a trustee, it is important to consider their ability to manage the trust effectively, which may require specific skills and experience in finance, law, or trust administration. A trustee can be a family member, friend, or a professional such as an attorney or a trust company, but it is crucial to assess their ability to fulfill the responsibilities of the role.

Evaluate financial literacy, availability, communication skills, impartiality, and proximity to trust property, especially Arizona real estate. Citadel Law Firm can review your trust document and help design trustee options for blended families, special needs beneficiaries, and high-value estates.

What Happens When a Successor Trustee Takes Over?

A common Chandler scenario is simple: a revocable living trust names the grantor as original trustee, then the grantor becomes incapacitated or dies in 2026, and the named successor trustee steps in.

Initial steps usually include obtaining a death certificate or medical incapacity documentation, reviewing the trust document, and formally accepting the role. The trustee is responsible for notifying financial institutions, updating titles, securing real property, maintaining insurance, and creating an inventory of all trust assets.

The successor trustee must separate trust assets from probate estate assets and may need to coordinate with an executor or personal representative. In the first 90 days, focus on securing property, notices, inventory, and cash flow. In the first 12 months, expect accountings, tax filings, distributions, and continuing trust management.

Early legal and tax advice is important because failure to uphold a trustee’s obligations can result in removal and personal financial liability for any losses to the trust.

Common Mistakes Trustees Make and How to Avoid Being Held Liable

Even careful family trustees can make errors that create personal financial risk and become personally liable.

Common mistakes include:

Commingling trust funds with personal accounts.

Making undocumented loans to beneficiaries.

Ignoring tax filings or required notices.

Failing to communicate with beneficiaries.

Leaving all assets in cash for years or speculating in high-risk investments inconsistent with the trust’s purposes.

Poor recordkeeping, including no receipts, no written distribution policies, and no annual summaries.

To reduce risk, use separate trust bank and brokerage accounts, create a written investment policy, send regular accountings, document every major decision, and use professional advisors. Working with an experienced trust administration attorney, like Citadel Law Firm in Arizona, is one of the best ways to avoid being held liable.

How Citadel Law Firm Helps Trustees and Families

Citadel Law Firm focuses on estate planning, wills and trusts, probate, and trust administration for clients in Chandler, Gilbert, Queen Creek, Mesa, and the wider East Valley.

For people creating trusts, Citadel Law Firm drafts a clear trust agreement, coordinates with financial planning professionals, and helps select the right trustee or successor trustee lineup. For new trustees, the firm reviews the trust, creates a step-by-step trust administration timeline, sets up recordkeeping systems, and coordinates with CPAs, financial advisors, and financial institutions.

The firm regularly advises on blended families, special needs beneficiaries, Arizona real estate portfolios, and multi-state asset ownership. If you need help understanding responsibilities, distributions, or trustee powers, schedule a free initial consultation in person in Chandler or remotely.

Frequently Asked Questions About How Trustees Work

Can a trustee change the terms of the trust?

Usually, no. A trustee must follow the trust document as written, especially when the trust is irrevocable. In a revocable living trust, the grantor usually retains amendment power while alive and competent. Limited court-approved changes may be possible, but an attorney should review the options.

Can a trustee be removed, and by whom?

A trustee may be removed under the trust document or by a court for breach of fiduciary duty, incapacity, conflict, or persistent failure to act. Beneficiaries, co-trustees, or a trust protector may be able to start the process. If you suspect serious misconduct, consult an estate planning lawyer promptly.

Is a trustee paid, and how are trustee fees determined?

Trustees are generally entitled to reasonable compensation unless the trust document says otherwise. Corporate trustees and trust companies often use published fee schedules, while individual trustees may charge hourly, flat, or percentage-based fees. Fees should be transparent and shown in accountings.

Do all trusts avoid probate if they have a trustee?

No. Assets properly titled in a funded revocable living trust usually avoid probate, but assets left outside the trust may still require probate. Naming a trustee is not enough; the grantor must retitle accounts and real estate during life.

When should I contact a lawyer if I have been named trustee?

Contact a trust administration lawyer as soon as you learn you are named as current or successor trustee, ideally before taking major actions. Early guidance helps prevent mistakes with tax filings, investments, distributions, and beneficiary communications. Arizona families can contact Citadel Law Firm for a free consultation about how does trustee work in their specific situation. Our trust attorneys will be pleased to help.

Meet Attorney David Gerszewski

Attorney David Gerszewski is specialized in Estate Planning, Trust & Probate Law and the founder of Citadel Law Firm PLLC. He is known for making legal matters easy to understand. His background in finance and tax law makes the estate planning strategies he designs for his clients just right. He was elected a Rising Star by Superlawyers.com 4 years in a row (2023-2026).

WE WOULD LOVE TO HEAR FROM YOU!

CALL US AT (480) 565-8020

Or use the button below to schedule your free estate planning consultation.