This article explains the difference between a will and a trust. This is not legal advice. If you need assistance, please schedule a free consultation.

The first thing to understand when planning the succession of your estate is the difference between a will and a trust. Both of these are legal tools that can be used to outline, among other critical decisions, how you would like your assets to be passed on after your death.

These two tools are very different, so to understand the difference between a will and a trust, you must have a basic understanding of what each offers.

A Will

A will, also known as a testament, is the more well known of these two tools. Despite this, there are many misconceptions about precisely what a will is, what it does, and how much power it has over your belongings.

Generally, the best way to think of a will is as a set of instructions about how you would like your belongings to be handled after you die. With a will, your bank accounts and property still need to be transferred to the name of your successors. To do this, a judicial process known as probate must be filed with the state of Arizona. A representative of the court will then consider your will as evidence of how they should distribute your belongings, as opposed to just using standard state laws.

Sign up to receive updates from our blog!

The probate process can take anywhere from 6 months to two years. Probate is also the time when creditors will make their claims for any debt that you did not pay before passing. During probate, your beneficiaries may have to pay for lawyers, court costs, appraisal costs, and other expenses. Costs can quickly add up during this process, especially if there are disputes between your beneficiaries.

In a way, this process can be compared to opening up a legal process against your own estate. Your inheritors may have to hire lawyers to represent them in court, present a will, and make sure that the court is allocating your belongings as you intended.

The benefit is that a will usually encompass all of your belongings. It can still make your intentions clear and it will help the court decide on your inheritors based on your wishes instead of state laws.

Problems may still arise if there are any ambiguities in your will and disagreements between your inheritors. You want to make sure that a will represents exactly what you want to happen, which is why it is always better to make one through an attorney instead of using templates.

A Trust

A trust is much more than a document. It is a private contract you set up to make an entity, some would compare it to a company that you set up to hold your belongings in a selective way. A car, for example, is normally registered under your name. If you wanted to put your car into the trust, it would be held under the name of the trust. The rules of the trust define who manages and who benefits from the assets that are held in the trust.

This may sound confusing at first. Thinking and comparing it to a company is a good way to start picturing it, however, keep in mind that, even though we will not get into it in this article, there are also some key differences between a trust and a company. One of the main benefits of a trust is that it is a private contract and so assets held in the trust avoid probate.

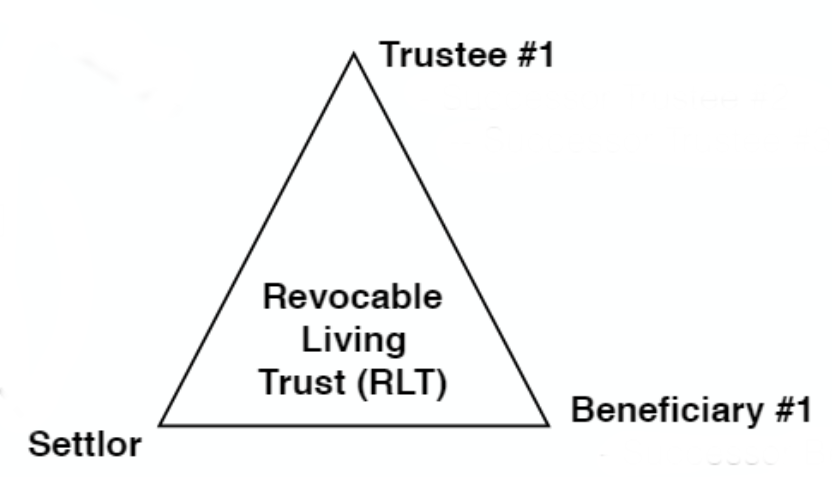

A trust has three core parts to it. These three “roles” can be taken on by one person, meaning that, while you are alive, you can be the Settlor, Trustee, and Beneficiary of a trust. For estate planning, the most basic type of trust is a revocable living trust. In this type of trust you would be in all three roles, but after you pass the rules of the trust will define who will take on each role. Please refer to the image below for a visual example. Here is an explanation of each of the roles:

Settlor: This is the person who arranges for the trust agreement and moves assets into the trust. The settlor creates the trust and defines the rules of how the assets within the trust should be managed.

Trustee: After the trust is written and assets are put into the name of the trust, the trustee manages those assets according to the guidelines in the trust agreement. A trustee is given fiduciary responsibility to distribute the property of the trust to the beneficiary. This person is expected to act in accordance with the rules of the trust and to prioritize the beneficiaries' needs. A good way to think of this would be as you think of a financial advisor. You give them control of your investments so that they can manage it; however, those are still your investments. If you are making a living trust, while you are alive you will usually be both the trustee and the beneficiary.

Beneficiary: This is the person who will "benefit" or receive the property of the trust. If you create a revocable living trust, you will most likely be the beneficiary while you are alive. There can be various beneficiaries to a trust, depending on how the trust is written. There can also be various rules set up in a trust so that a successor beneficiary only receives the property after a certain amount of time or under certain circumstances.

As you have probably noticed, there are a lot of hypotheticals involved in my description of a trust. This is because you have complete flexibility over the rules of the trust and how it is created. While this makes it harder to explain, it is one of the main benefits of a trust as it means that you can customize a trust to fit your specific needs and the needs of your family.

I also mentioned the term living trust various times. This is because you may consider setting up a trust while you are alive and you want to be the person in the aforementioned roles to during your lifetime.

If you were to become incapacitated or pass away, the trust agreement designates a successor trustee who would step into your role as a trustee. This person would assume responsibility for managing the trust and distributing your assets and property to you or your designated successor beneficiaries, according to the rules outlined in the trust. This person is given fiduciary responsibility which means that, if they were to violate terms of the trust, the interest of the beneficiary, or take the assets for themselves, they could be subject to civil and/or criminal penalties.

A trust is more complex than a will, and it costs more money to set up. It also only manages assets that are transferred to that trust. While the cost of setting up a trust can be higher upfront, it can also save money and time for your successor beneficiaries and even protect your estate from their creditors. A trust also offers privacy since it does not go through probate and is not part of a public record.

You should now have a basic understanding of what a will and a trust is and the differences between them. If you have further questions, please do not hesitate to reach out or schedule a free initial consultation to speak directly to an attorney.

If you need legal assistance, please schedule a free consultation today. Our attorneys practice Estate Planning law and look forward to working with you.

To know more about Wills also read our blog article "What happens if I die without a Will in Arizona?", "What is a Living Will?", "What is a Will?" and "Does a Will avoid probate?".

{kind=link}